Author: Maia Benstead, Technology Analyst at IDTechEx

Thin film photovoltaics (PV) currently comprises a small portion of the total solar market, yet offer extensive opportunities for applying solar power in new and emerging applications. Many types of this technology offer design simplicity, ease of manufacturing, as well as cost competitiveness with silicon, making it well suited to high volume production. Despite these advantages, thin film PV has struggled to gain the same market foothold as silicon-based solar panels. The key questions remain: why has thin film PV lagged behind, and what factors could help it become more competitive in the solar industry?

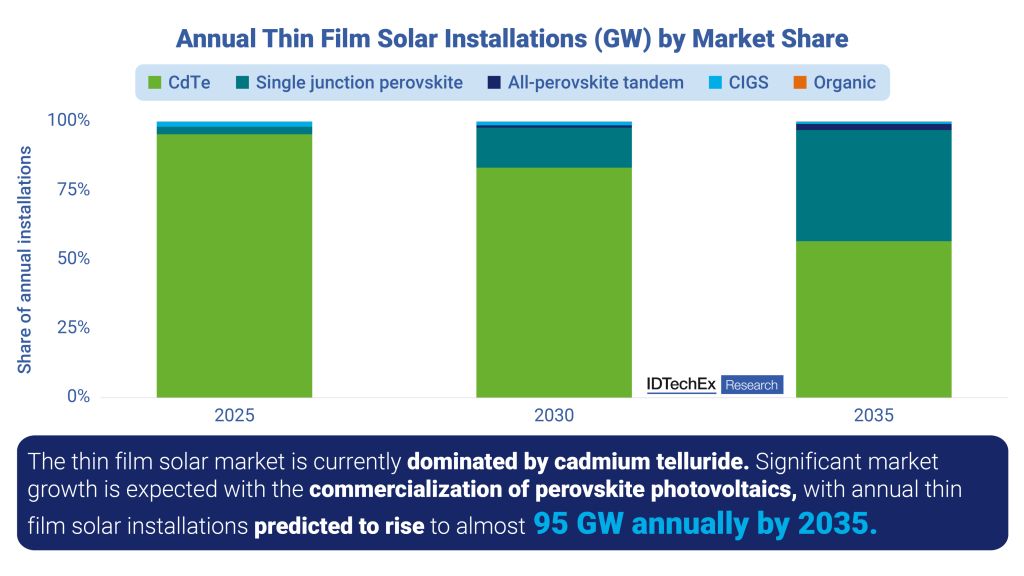

Annual thin film solar installations (GW) by market share. Source: IDTechEx

IDTechEx's report, “Thin Film Photovoltaics Market 2025-2035: Technologies, Players, and Trends“, provides a deep dive into the entire thin film PV sector, analyzing the technologies, applications, and market players targeting its uptake. The report extensively covers the entire thin film PV market technologies, including dye-sensitized solar cells (DSSC), organic photovoltaics (OPV), perovskite PV, cadmium telluride (CdTe), copper indium gallium selenide (CIGS), gallium arsenide (GaAs), amorphous silicon (a-Si), and copper zinc tin sulfide (CZTS). Profiles of over 35 key market players and a detailed assessment of major applications such as solar farms, residential rooftops, building-integrated PV (BIPV), and wireless electronics help to formulate granular 10-year forecasts for the entire solar market. IDTechEx forecasts that the thin film PV market will surpass US$11 billion by 2035, with growth largely driven by the rise of a new thin film solar technology.

CdTe PV continues to dominate the thin film solar market

Cadmium telluride (CdTe) PV remains the dominant thin film solar technology and is the second most widely used solar technology after silicon. This technology has been researched since the 1950s, with modules first brought to market in the early 2000s. CdTe PV modules offer the same longevity as silicon modules (~25 years), and despite its smaller scale of production, they are very cost competitive. Additionally, due to a straightforward, relatively low temperature, and automated manufacturing process, CdTe solar modules boast an energy payback time of less than a year.

Unlike silicon PV, which is heavily reliant on China's supply chain, CdTe PV production is largely centered in the United States (US), where it has benefited significantly from policy incentives. First Solar, the largest CdTe manufacturer, accounts for over 90% of global CdTe PV production, with the US being the largest market for this technology, contributing over 30% of its utility-scale solar capacity. The 2022 Inflation Reduction Act (IRA) has further driven CdTe PV expansion by incentivizing domestic PV manufacturing, and with the uncertainty in global import tariffs, US-based CdTe PV production is likely to grow even further.

Despite its advantages, however, CdTe PV does face some challenges. The primary concern is the scarcity of tellurium, a rare element crucial for CdTe solar cells. Future shortages could lead to price volatility and restrict production capacity. In 2023, 640 metric tons of refined tellurium were produced, up from 584 metric tons in 2022, with demand continuing to rise due to its use in both growing PV and thermoelectric markets. In response, First Solar has introduced a global recycling initiative to recover 90% of materials from used modules, including CdTe absorber layers and glass substrates. While current tellurium recycling rates remain low due to the long lifespan of solar modules, early deployments reaching end-of-life from 2025 onward will likely boost the secondary tellurium supply.

Despite its longevity and cost efficiency, CdTe PV is unlikely to challenge silicon PV on a large scale. However, IDTechEx forecasts that CdTe will continue to dominate the thin film solar market, at least until the rise of a new, and highly promising technology begins to shift the landscape.

Perovskite PV to boost the thin film solar market and compete with CdTe PV

Perovskite PV is an emerging thin film solar technology that has garnered substantial academic and industry attention. This technology fundamentally operates similarly to both CdTe and silicon PV technologies but makes use of a perovskite-based semiconductor as the active layer. Perovskites are a class of materials with a cubic crystal structure in the form ABX3. In semiconducting perovskites, the A-site contains large organic cations (such as methylammonium or formamidinium), the B-site features lead or tin, and the X-site consists of halide ions.

Fabrication of perovskite solar cells is both sheet-to-sheet or roll-to-roll compatible, allowing for scalable and automated manufacturing, which is highly attractive from a financial perspective. Perovskite synthesis also requires relatively abundant and inexpensive raw materials, again helping to considerably lower manufacturing costs. By the end of the decade, IDTechEx finds that perovskite PV will be substantially lower in cost than both alternative thin film technologies as well as silicon PV, accelerating its commercial adoption.

Beyond single-junction perovskite cells, researchers are exploring tandem device architectures to push efficiency levels even higher. Single-junction technologies, including silicon, CdTe, or alternative thin films, are approaching a theoretical efficiency limit of around 30%. To overcome this limitation, perovskites can be integrated with other solar materials to create multi-junction cells, which can achieve theoretical efficiencies of up to 43%. Among the most promising tandem technologies gaining commercial interest are perovskite/silicon and all-perovskite PV. The nature of perovskite PV means that it minimally impacts the overall mechanical properties of the underlying solar device.

Perovskite photovoltaics are beginning to enter early-stage commercialization, with many industry leaders recognizing them as the next major breakthrough in solar technology. The rapid pace of innovation, growing investment, and the projected expansion of the perovskite PV market are helping to boost the thin film solar sector. IDTechEx finds that by 2035, perovskite PV will make up over 40% of all thin film solar installations, signaling a major shift in the industry.

For further details on perovskite photovoltaics and alternative thin film solar technologies, see IDTechEx's report, “Thin Film Photovoltaics Market 2025-2035: Technologies, Players, and Trends“. Downloadable sample pages are available for this report.

For the full portfolio of energy and decarbonization market research available from IDTechEx, please visit www.IDTechEx.com/Research/Energy.