Author: Dr Alex Holland, Research Director at IDTechEx

The global market for Li-ion battery cells alone is forecast to exceed US$400 billion by 2035, driven primarily by demand for battery electric cars and vehicles. Improvements to battery performance and cost are required to ensure widespread deployment of electric vehicles, enable the electrification of other vehicle modes such as air taxis, and to enable longer runtime and functionality of electronic devices and tools, leading to strong competition in developing next-generation Li-ion technologies. The IDTechEx report, “Advanced Li-ion Batteries 2025-2035: Technologies, Players, Markets, Forecasts” provides an in-depth analysis and discussion on the trends and developments in advanced and next-generation Li-ion cell materials and designs, including for silicon anodes, Li-metal anodes, cathode materials (e.g. LMFP, Li-Mn-rich, sulfur) and cathode synthesis innovations, and an introduction to solid-state batteries, amongst other areas of development. Key players and start-ups in each technology space are identified and profiled.

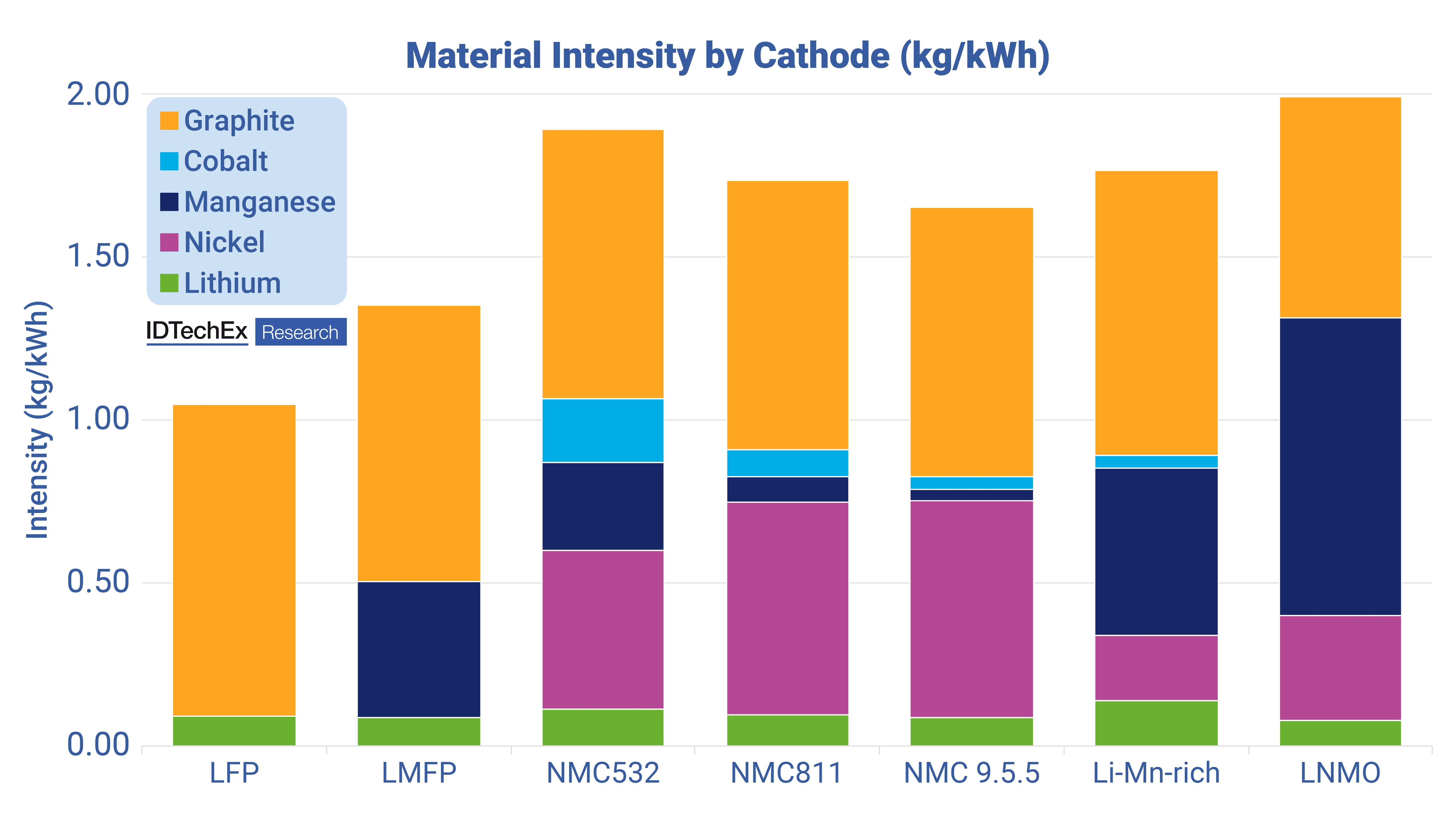

Supply and material criticality

In March 2025, the EU Commission announced that it would be funding 47 strategic raw materials projects across Europe, with 30 of these involving lithium, graphite, nickel, cobalt, and/or manganese. This highlights the ongoing importance of the battery supply chain, as well as concerns of over-reliance on one source for the supply of various critical materials. LFP (lithium iron phosphate) type Li-ion batteries negate the use of cobalt and nickel and have emerged as the dominant choice for stationary energy storage systems, while its adoption in the EV sector is also increasing, driven by its low cost. However, the LFP supply chain is dominated by China, with effectively all LFP cathode material produced in the country. Alternative low-cost cathode chemistries may, therefore, be needed to shift this reliance. Options include LMFP, Li-Mn-rich, and zero-cobalt layered oxides. These cathode chemistries will be important for diversifying supply chains and bridging the gap between the low cost of LFP and the high energy density of NMC and NCA while also impacting demand for materials such as cobalt, nickel, and even lithium. IDTechEx's report provides an appraisal of the various next-generation Li-ion cathode materials, highlighting their respective strengths and weaknesses and the value proposition they offer.

Intensity of key materials in different Li-ion cell chemistries. Source: IDTechEx

Protectionist policies from the United States, coupled with aspirations for “energy dominance”, further emphasize the importance of securing diversified and sustainable supply chains. Initiatives aimed at localizing battery material production and reducing reliance on Chinese-dominated supply chains are gaining momentum across various regions, with both government and private sector investments accelerating the development of alternative material sources and next-generation battery technologies.

Competing with next-gen technology

Competing with Chinese giants such as CATL and BYD and Korean and Japanese manufacturers including LG ES, Samsung SDI, SK On, and Panasonic will continue to prove challenging, highlighted by ongoing difficulties from start-up battery manufacturers with Northvolt offering a prominent example. Despite a highly competitive environment, the US and Europe are home to many start-ups developing advanced and next-generation battery technologies, ranging from silicon anodes and next-generation cathodes to solid-state batteries and alternative routes to cathode synthesis. Leapfrogging the current generation of Li-ion battery technology offers one of the most promising routes to capturing a foothold in the burgeoning battery market.

Higher energy density, faster charging batteries

Advanced and next-generation Li-ion technologies will also be key to further enhancing the performance of Li-ion batteries. One of the most promising innovations is the integration of silicon-carbon composite anodes into commercial batteries to increase energy density, allowing for longer-lasting battery life and more compact cell designs. Many silicon anode developers are also reporting improvements to rate capability and fast charging times through the use of silicon anode materials. Deployment of silicon-carbon materials at higher weight percentages has already begun in smartphones and other consumer electronics, with these high-performance anodes now poised for adoption in EVs. The use of higher amounts of silicon material in anodes could also play a role in reducing demand for graphite, where potential restrictions on graphite exports from China provide another example of the importance of next-generation and alternative battery technologies in diversifying supply chains.

IDTechEx's report, “Advanced Li-ion Batteries 2025-2035: Technologies, Players, Markets, Forecasts”, appraises the various next-generation Li-ion technologies being developed and commercialized. This report covers and analyzes many of the key technological advancements in advanced and next-generation Li-ion batteries, including silicon and lithium-metal anodes, manganese-rich cathodes, ultra-high nickel NMC, LMFP, lithium-sulfur batteries, as well as optimised cell and battery designs. Addressable markets and forecasts are outlined and provided for next-generation anode and cathode materials.

For more information on this report, including downloadable sample pages, please visit www.IDTechEx.com/AdvLithium.

For the full portfolio of batteries and energy storage market research available from IDTechEx, please see www.IDTechEx.com/Research/ES.