Author: Dr Jiayi Cen, Technology Analyst at IDTechEx

The Direct Lithium Extraction (DLE) market has witnessed a surge in interest from a diverse range of industries, including mining, water treatment, oil and gas, chemicals, and engineering. This convergence of diverse entities into the DLE space reflects the technology's potential to revolutionize lithium production, a crucial component in the global transition towards renewable energy and electric transportation. The appeal of DLE lies not only in its ability to enhance the efficiency and sustainability of lithium extraction but also in its potential to unlock new resources and reshape the global lithium supply chain. IDTechEx’s report on the topic, “Direct Lithium Extraction 2025-2035: Technologies, Players, Markets and Forecasts”, predicts DLE to disrupt the brine mining market, with a compound annual growth rate (CAGR) of 19.6%, making it the fastest-growing segment in the industry.

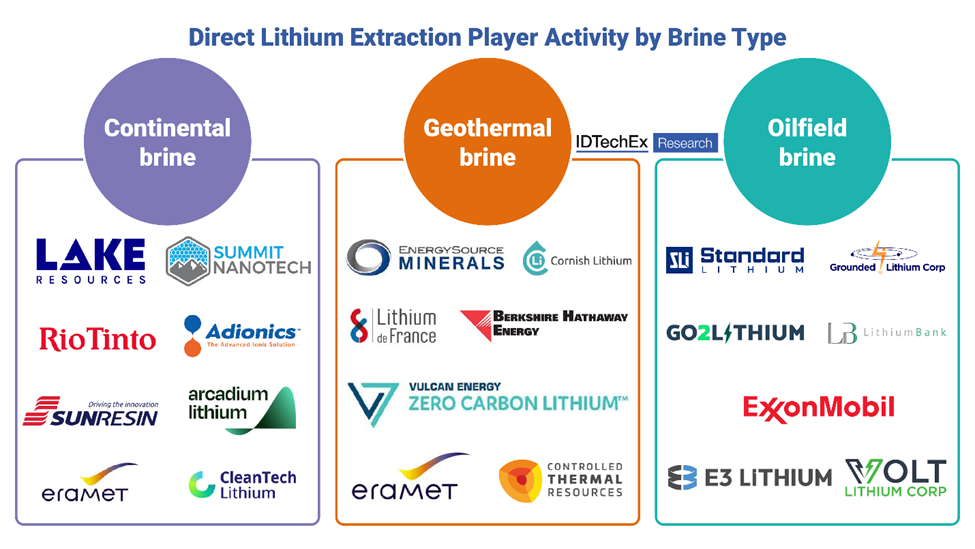

From salt flats to oilfields, lithium brine resources exist along a diverse spectrum, each with its own set of advantages and challenges. This diversity draws interest from DLE players across various industries as they seek to capitalize on the unique opportunities these resources present.

DLE players (including lithium producers, resource developers/owners and DLE technology developers) activity by brine type. Note that some players are engaged in lithium extraction from multiple types of brine resources. Source: IDTechEx

Continental brines form the primary and most exploited source of lithium. The “lithium triangle”, encompassing regions of Bolivia, Chile, and Argentina, is home to vast lithium deposits. South American brines are highly valued for their rich lithium content and proven effectiveness in traditional evaporation-based extraction methods. These brines often have high lithium concentrations, making them economically attractive for lithium extraction. Leading lithium producers like SQM, Albemarle, and Arcadium Lithium are extracting lithium from this type of brine. Consequently, continental brines in South America have garnered interest from DLE players such as Adionics, Summit Nanotech, and CleanTech Lithium. Despite the high abundance of continental brines, applying DLE to these resources faces several challenges. For example, many deposits are located at high altitudes, creating complex logistics for transporting large equipment and materials. The lack of pre-existing infrastructure in some areas further complicates operations.

Geothermal brines are naturally hot and rich in minerals and dissolved metals. A key benefit of geothermal resources is the potential for integrated, low-carbon operations. Geothermal energy can power both lithium extraction and refining processes. Several geothermal DLE players intend to produce lithium hydroxide, a more energy-intensive lithium product than lithium carbonate, used for the synthesis of high nickel layered oxide cathodes. Moreover, the co-production of heat and power as by-products diversifies revenue streams, reducing players’ vulnerability to lithium price fluctuations. Players in the field include Vulcan Energy Resources, which is advancing the Zero Carbon Lithium project in Upper Rhine Valley, Germany. Lithium de France is exploring geothermal areas in Northern Alsace, France, and is backed by investors, including Equinor, an international energy company. Geothermal brines found in regions like Europe and the United States offer the advantage of being located near local battery manufacturers. This helps localize the lithium supply chain. Moreover, these regions typically exhibit lower sovereign risk, which provides a more stable environment for project development and investment. However, geothermal lithium extraction faces unique challenges, such as high brine temperature and complex composition, which can pose technical hurdles.

Oilfield brines found in underground petroleum reservoirs represent another promising frontier in lithium extraction, with significant deposits in regions like Arkansas and East Texas in the USA, and Alberta, Canada. These resources, along with produced water from oil and gas operations, offer unique advantages. The primary benefits include the utilization of existing processes and facilities, streamlining permit acquisition, and reducing the need for new asset development, which can potentially accelerate project development. Additionally, oilfields often provide access to cheaper power sources, with some players like E3 Lithium and Volt Lithium Corp leveraging cogeneration plants to reduce energy costs further. The potential to leverage existing infrastructure and resources has also attracted players from the oil and gas industry in entering the DLE market.

The oil and gas sector's foray into lithium extraction is primarily driven by two factors: (i) the opportunity to apply their geology and processing expertise on lithium extraction from brines to support the renewable energy transition and (ii) the potential to derive value from by-products and existing infrastructure. This approach is redefining resource value, particularly for produced water, opening new revenue streams and promoting responsible water management. Partnerships like E3 Lithium with Imperial Oil to redevelop historic oil fields in Canada, and Equinor's collaboration with Standard Lithium in the USA, exemplify this trend. However, challenges remain in this area, with one of them being the lower lithium concentrations in oilfield brines and produced water in general. Efficiently and economically extracting lithium from these lower-grade sources presents a technical and financial hurdle, driving ongoing innovation in extraction technologies.

Players may enter the DLE market with different approaches, leveraging characteristics of different brine resources. This has led to the development of customized DLE technologies and lithium recovery processes designed to optimize lithium extraction and production from different types of brine sources. Recognizing the complexity and potential of this field, many organizations are forming partnerships to accelerate the development and deployment of DLE technologies. These collaborations often bring together complementary expertise. This trend towards customization and collaboration reflects the industry's response to the challenges and opportunities presented by different lithium brines. It also suggests the sector's dynamic nature, where adaptability and strategic alliances play crucial roles in advancing DLE technology and bringing it to commercial scale.

The IDTechEx report, “Direct Lithium Extraction 2025-2035: Technologies, Players, Markets and Forecasts”, offers a comprehensive analysis of DLE technologies, trends, and regulatory frameworks in countries with major lithium brine deposits. Additionally, it provides detailed projections for DLE, segmented by technology, country, and brine types, offering a holistic view of the evolving lithium extraction landscape.

To find out more about this report, including downloadable sample pages, please visit www.IDTechEx.com/LithiumExtraction.

For the full portfolio of energy storage market research available from IDTechEx, please see www.IDTechEx.com/Research/ES.